The old analogy that you should never put all your eggs in one basket is highly important when it comes to investing. If one part of your portfolio slides, another may outperform, which should provide overall balance – and hopefully grow your wealth.

With global diversification key for success, Dan Brocklebank, UK head at Orbis Investments, warns that many people who think they’ve spread their capital are unaware of just how highly correlated holdings may be, and ultimately, how skewed markets are.

“Risk can creep up on people without them realising”, he warns, emphasising that the framework around diversification truly matters because of today’s context.

Correlation in today’s context

He explains that the ‘Magnificent Seven’ (Tesla, Meta, Amazon, Alphabet, Nvidia, Apple and Microsoft) make up nearly 20% of the World Index, but only make up 11% of the profits. Naturally, we’d presume they’d contribute the equivalent, around 20%.

To put that market concentration in perspective, the seven companies that make up the ‘Magnificent Seven’ are, when combined, worth more than ALL the companies listed on the five largest stock markets outside the US. Combined, these companies contribute 25% of global profits, so expectations for growth from these companies are much lower than the ‘Magnificent Seven’.

Wellness and wellbeing holidays: Travel insurance is essential for your peace of mind

Out of the pandemic lockdowns, there’s a greater emphasis on wellbeing and wellness, with

Sponsored by Post Office

Another way to highlight this is to look at how sensitive each company in the FTSE World Index is to the economy (how cyclical they are) and how expensive they are (the valuation).

When dividing up the whole market universe to give a view of how cheap and how cyclical stocks are, they’re fairly evenly spread across value cyclical and value defensive stocks, as well as growth defensive and growth cyclical stocks.

But this data misses out the relative importance of each company, so once this is included, it paints another picture.

Brocklebank explains that when you buy an index, you’re not buying an equal proportion of each company, as they’re weighted based on their value.

So once market cap is reflected, “there’s a significant concentration of market value in the bottom-right-hand quadrant [that] contains the defensive growth names,” he explains.

Source: Orbis

“Seven of those are the ‘Magnificent Seven’, but there’s still a huge number of large blobs in that bottom-right-hand corner, so it’s not just seven stocks, it’s actually a skew in the overall market,” Brocklebank says.

He adds: “Actually 60% of the World Index is in that bottom right hand quadrant. If it was genuinely evenly distributed across the four quadrants, you’d expect 25% in each.”

Initially when reviewing these findings, Brocklebank says he thought these “look extreme”, so he wanted to check whether there has always been a concentration, and whether “markets are just like that”.

However, when looking at this data over time (since 1993), he found this has been very different. It has been as low as 20%, and almost as high as today (mid-50s) back in the late 1990s. “But even then, it wasn’t as high as it is right now,” he says.

Source: Orbis

Brocklebank says: “We know that history doesn’t repeat itself, but it rhymes, so we asked how investors did in the late 1990s when the weighting in that quadrant was last near today’s levels. Any market history will show you it worked for a bit then suddenly it went really pear-shaped for a while, which rings alarm bells – maybe we have history rhyming here, which is something to think about when it comes to risk.”

Does this skew matter to UK investors?

The next step for Obis was to determine exactly how this skew could impact UK investors, based on how their portfolios are currently positioned.

And so, the investment firm looked at the positioning of UK investors, based on the largest funds in the Investment Association Mixed 40-85% shares sector. Here it found over 50% of investor pounds is invested in passive strategies.

“That means the equity portion [of the 60% equity/40% bond asset allocation strategy] is going to mirror that concentration as by definition, they’re buying the benchmark”, Brocklebank explains.

He adds: “So, at least half have that skew in their equity portfolio to the defensive growth quadrant.”

Meanwhile, 34% is invested in active funds, of which 63% is invested in funds that have a growth mandate.

Brocklebank says: “Basically, those are active funds that are only picking from the right-hand column [growth cyclical or growth defensive].”

Meanwhile, 31% of the actives are in a ‘blend’, so Brocklebank says “it’s reasonable to assume they will average out at the benchmark”.

“Only a minority of the minority are targeting the value space in markets at the moment [the left-hand column],” Brocklebank says.

‘Skewed in practice, not just a theoretical problem’

He adds: “There’s quite a compelling case if you look at the funds positioning data that investors’ portfolios are skewed in practice; it’s not just a theoretical problem for the make-up of the index, as that’s actually flowing into portfolios.”

Another way of seeing this problem is by looking at the correlations of the largest funds. Orbis looked at the 10 largest funds in the IA mixed 40-85% shares sector.

For the top funds, how much of their movements are statistically the same averages at over 90%, and so even if your investments are spread over these top 10 funds in this space, while “you may feel diversified”, they’re also at over 90%.

He says: “The key thing about diversification and for it to work, your holdings need to perform differently. If you own 10 property stocks, they’re all going to behave fairly similarly based on how the property sector does.

“In essence, you’ve a situation where the industry is herding towards – in effect – the benchmark where correlations are very high.

“It’s very easy for investors to have fallen into this trap because the industry’s not really offering them any diversification. The big funds are so similar.”

Source: Orbis

Investors sought stability

According to Juliet Schooling Latter, research director at FundCalibre, central bank interest rate hikes aimed at curbing inflation have likely influenced the trend of a small group of companies holding a very large share of the overall value.

“In this environment, investors are seeking stability, which has led them to established, large companies perceived as less risky than smaller or newer ventures.

“Passive products surged in popularity thanks to their low fee structures and relative outperformance of active funds. It’s been a sound investment strategy,” she says.

But Schooling Latter adds there are potential risks.

“The S&P 500 currently holds about 28% of its market cap in the so-called ‘Magnificent Seven’ stocks, exceeding concentration levels observed even at the peak of the late 1990s dot-com bubble. This concentration risk transcends US borders due to the nation’s dominant position on the global stage – the MSCI World Index, encompassing over 1,500 companies across 23 developed markets, has over 18% of its market cap tied to just five US technology giants.

“Unbeknownst to many investors, multi-asset funds heavily invested in these indices rely disproportionately on a handful of US tech giants for returns. This concentration likely contributes to the correlation between the top 10 largest funds within the sector.”

What’s the solution for investors?

Brocklebank compares the Orbis OEIC Global Balanced Fund, which has a much smaller correlation, from 0.49 to 0.7 against the 10 largest funds.

He explains that the fund is ‘bottom up’ and looks for cheap investments, starting with the simple view that if they can find companies that are trading at an attractive starting valuation, then it’s likely to generate better returns over long periods of time.

“If we do that, given the way everything’s positioned, then we should help people provide some counter balance to their portfolios,” Brocklebank says.

Meanwhile, starting valuations are hugely important to investors, and so the US is very expensive relative to history, while the rest of the world looks quite cheap.

“That gives you an opportunity to re-position. We all know the index is at record highs in the US – up 66% – which is also where the market is skewing towards,” he says.

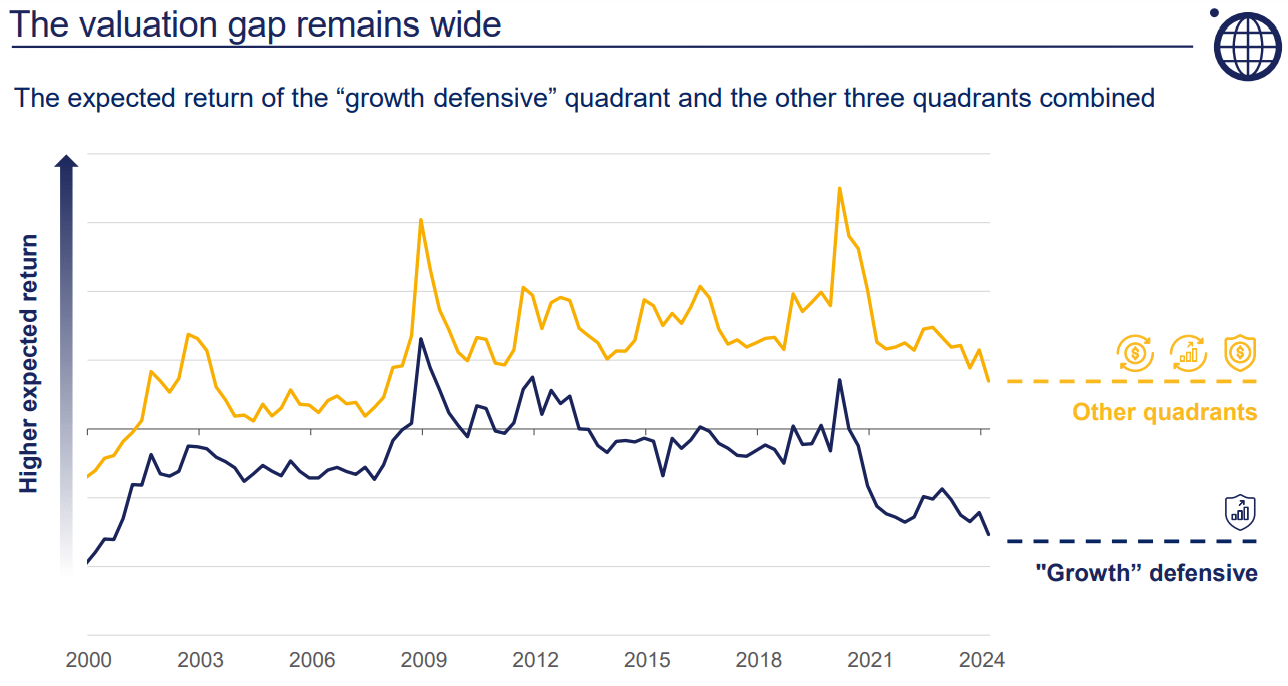

At the same time, the growth defensive quadrant also has the lowest expected return it’s ever had, Brocklebank says.

Meanwhile, the same expected returns for the other quadrants shows that the rest of the market “looks to have quite reasonable expected returns”.

Source: Orbis

By buying the index, an investor is essentially buying what did well in the past, Schooling Latter explains.

“However, the future may unfold differently, with different stocks and sectors outperforming. An active manager is not constrained to the past composition and can have a more forward-looking view, overweighting areas they believe to be undervalued and will do well going forward,” she says.

She adds that for truly global diversification, investors should consider actively managed funds with a focus on regions beyond the US.

For instance, European and UK equities “currently present a compelling opportunity”.

“Their historically low valuations offer significant upside potential, particularly for value-oriented funds. Consider the Marlborough European Special Situations Fund for European exposure and Schroder Recovery for UK exposure.

“Both funds are well-positioned for potential re-ratings and will complement any global growth exposure within a diversified portfolio,” she says.

Meanwhile, Asia “boasts a diverse range of exciting investment themes”, from the rapid growth in India, to the resource wealth of Australia, to the technology might of Taiwan and Korea, she explains.

“Here, we suggest FSSA Asia Focus or, for exposure to the region’s established dividend payers, consider Schroder Oriental Income.”

Meanwhile for investors seeking a passive alternative for diversified global exposure, Schooling Latter says investors could consider an equally weighted index.

“By assigning equal weight to each constituent, such indices ensure a balanced representation of stocks across the market. This mitigates size bias, benefiting investors by capturing the potential of emerging growth companies that may be under-represented in market cap-weighted indexes,” she explains.

The 10 largest funds in the IA mixed 40-85% sector, source FEfundinfo: